With imports accounting for 70 percent of Egypt’s trade, the country relies on dollars. Those greenbacks are increasingly being borrowed from international markets because foreign direct investment declined by 23.5 percent in fiscal year (FY) 2018/2019 compared to the previous year. Based on Central Bank of Egypt (CBE) data, dollar-denominated debt represented 14.4 percent of GDP in 2015; the figure reached 37 percent by 2018.

Accordingly, news reports of a global shortage of American currency should worry Egypt’s private sector, government and the CBE. A Reuters story published in mid-November, reported that there is only $3.2 trillion in circulation worldwide. That compares to $7 trillion in June 2018, as reported by the International Monetary Fund. That means international lenders and borrowers of dollars could be “dangerously exposed should U.S. lenders stop feeding the system, even temporarily,” noted the Reuters story.

International markets got a taste of how expensive such a shortage could be when the U.S. Federal Reserve (Fed) lending rate to commercial banks, known as the repo rate, spiked in September from 2 percent to 7.5 percent, dropping only after the Fed pumped more than $180 billion into international markets between September 27 and October 10, according to a Business Insider story. “It affected us in the FX […] market a great deal. There was a lot of panics, spreads widening, increased volatility,” James Topham, a trader at Canadian bank BMO, told Reuters. At press time, the Fed’s repo rate was 1.63 percent.

As a result, some experts are looking to cryptocurrency as a possible alternative to the dollar. “Bitcoin could be a fine substitution for the [dollar], which the Fed has turned into a bubble,” said U.S. Sen. Rand Paul in May as reported by cryptocurrency website U.Today. That opens the door to “radically changing” how non-U.S. businesses finance trade among themselves, wrote Noelle Acheson, a member of CoinDesk’s product team, in an August blog post.

Securing the greenback

The greenback became the de facto currency for international trade in 1944, when 44 countries agreed to peg their currencies to the value of the dollar, which was pegged to gold. The status of the American currency in international trade didn’t change after it was decoupled from gold in 1971 because the United States remains the world’s biggest economy.

The most straightforward way to access dollars is to export to the United States. According to the CBE, Egypt’s exports increased to $2.856 billion in FY 2018/2019 from $2.08 billion a year earlier. Another solution is for nations to sell dollar-denominated treasury debt. Egypt’s government reportedly plans to issue $3 billion to $7 billion in dollar-denominated bonds by the end of FY 2019/2020, Egypt Today reported in October. The downside is that repayment of the principal and interest on such bonds must also be in dollars.

A third way to obtain the greenback is through U.S. companies investing abroad. For Egypt, that source is tightening as non-oil American foreign direct investment dropped 27.3 percent in FY 2018/2019 compared to the previous year to $1.63 billion, according to the CBE.

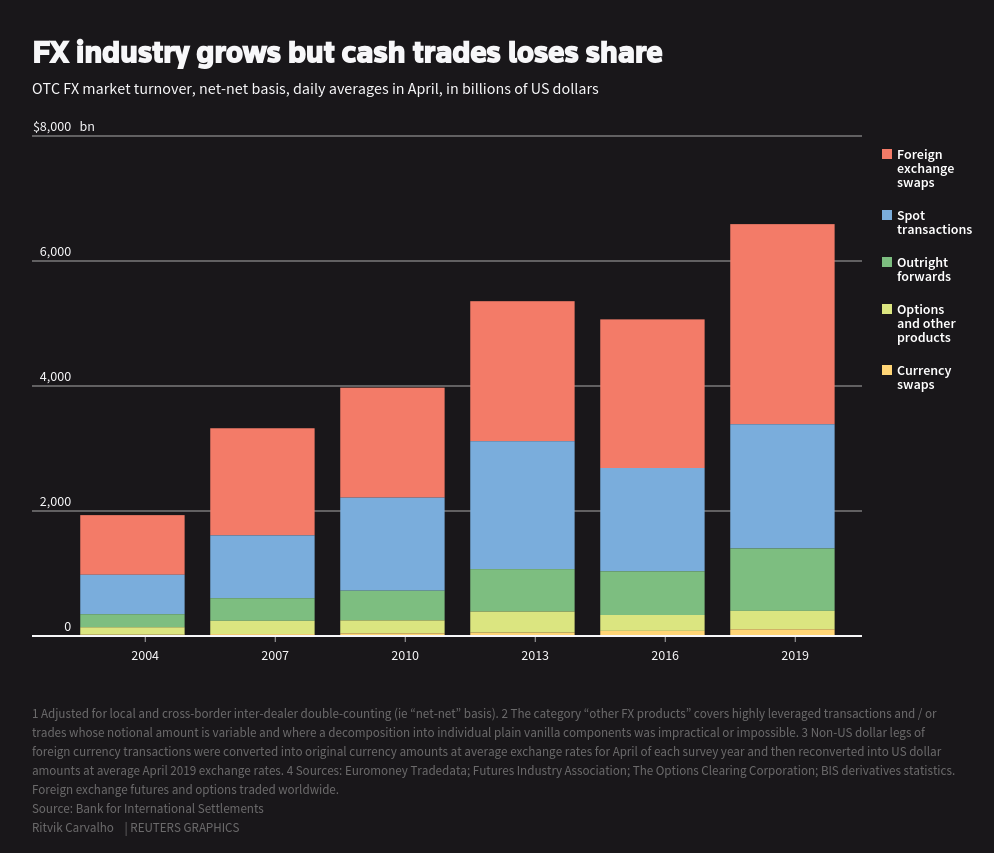

However, the most common way to secure dollars is via the international “swap market.” In it, a company can agree with an American investor to “swap” cash based on the prevailing dollar exchange rate. For example, a company in Egypt can give EGP 16.2 million, whose interbank overnight interest rate is 12.25 percent, to a U.S. investor in exchange for $1 million at an interest rate of 1.75 percent.

Throughout the swap, Egyptian businesses pay the American investor the dollar interest rate plus a “swap” markup, based on the demand for dollars. Meanwhile, U.S. investors pay the CBE’s overnight rate.

In such an arrangement, both parties win. Egyptian businesses pay only the Fed interest rate plus the markup. That will always be lower than what local banks charge for loans, whether in Egyptian pounds or dollars, says an anonymous teller at an Egypt-based international bank. The American party makes money from the markup as well as investing in treasury debt whose yields exceed CBE rates.

According to Tobias Adrian, director of the monetary and capital markets department at the IMF, the global financing gap is between $1.4 trillion and $1.5 trillion compared to $1 trillion in 2008. “Much of that has to be funded in FX swap markets,” Adrian told Reuters in November.

Shortage problem

The number of dollars in circulation worldwide has shrunk by more than half since 2014, according to an IMF report this year. That made the dollar’s global lending markup jump from 0.1 percent in 2014 to 1.63 percent on November 22, according to Trading Economics aggregator. That mirrored a rise in the dollar index from 80 points to nearly 100 points between 2014 and November 22, according to Trading Economics. Both indicators reflect the dollar’s value when it comes to funding non-U.S. trade.

According to a Reuters story in November, a primary reason for this shortage is that Fed regulations now require American banks to hold 8 percent of their capital in reserve to help protect them from insolvency. The article also cited trade wars that limit U.S. banks’ business abroad and U.S. companies that are increasingly investing in their home country. An IMF blog post last year blamed a new law that encourages companies to repatriate profits.

“These developments are taking place against the backdrop of the Federal Reserve’s interest rate increases and gradual reduction of securities holdings on its balance sheet, which would ultimately lift funding costs for all borrowers,” according to the IMF blog post.

Forty-nine percent of trade not involving the United States was in dollars last August compared to 42 percent in 2013. The other problem is the rising need for dollars to fund non-U.S. trade, according to Reuters, citing the Bank for International Settlements,

New system?

Uncertainty over the supply of dollars in the wake of America’s protectionist policies and unwillingness to import goods has led some to question whether they should continue to rely on the greenback as the global reserve currency. “In short, the cost of dollar borrowing is likely to become more volatile and perhaps more sensitive to changes in U.S. monetary conditions and global risk appetite,” said a 2019 IMF report referenced by the Financial Times in November.

Some economists say now would be an excellent time to use the IMF’s Special Drawing Rights basket as the world’s reserve currency. The dollar accounts for 41.73 percent of the basket, the Euro 30.93 percent, the Yuan 10.92 percent, Yen 8.33 percent and British Pound 8.09 percent. The Egyptian pound’s exchange rate to the basket is EGP 22.16 to SDR 1 as of November 24.

Acheson of CoinDesk doubts the IMF’s unified currency could replace the dollar. “Even a liquid SDR in its current configuration would be subject to national priorities and vulnerabilities,” she wrote in her blog. “A sharp depreciation in the U.S. dollar as central banks switch to the SDR as a reserve holding could destabilize the basket.”

Acheson also doubts that cryptocurrencies, including Bitcoin, could take the dollar’s place. “Bitcoin will not become a universal settlement token for trading contracts,” she wrote, citing its volatility. In addition, she thinks it is unlikely that businesses and sovereign powers would give up their central bank-controlled currencies for an unregulated one.

However, she says the integration of cryptocurrencies into trade could change how companies and countries interact, suggesting such a change might occur with the introduction of Facebook’s Libra cryptocurrency, which is pegged to a basket of currencies and government debt. It could act as a “dollar” for cryptocurrencies. She also cited a 2010 story by The Economist concluding it would be “too difficult to attempt” reorganizing the world’s currencies.

“The biggest risk to the world economy right now [is] not trade tension, overvalued assets or negative yields,” wrote Acheson. “It’s complacency in assuming that the status quo will hold. Profound change always costs a massive amount of political and economic capital, but it happens regardless.”

{kind=link}