As global supply chains grapple with the effective closure of the Strait of Hormuz, a critical energy and trade artery, logistics operators are urgently seeking alternative routes. One corridor rapidly gaining prominence is the land and sea link between Egypt’s Safaga port and Saudi Arabia’s Duba port.

In an interview with Business Monthly, Egytrans CEO Abir Leheta outlined what the disruption means for Egypt, the readiness of the private sector, and the strategic steps needed to transform this short-term solution into a long-term economic advantage.

![]()

Global Shock Drives Rerouting![]()

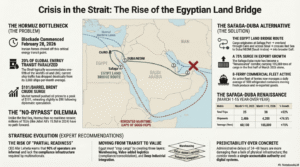

The shift toward the Safaga–Duba corridor follows a severe bottleneck in the Gulf. According to BBC, Iran has blockaded the Strait of Hormuz since February 28, disrupting a route that typically carries around 20% of the world’s oil and liquefied natural gas. Ship traffic has dropped sharply from its usual 3,000 vessels per month amid threats targeting commercial shipping.

The disruption has triggered volatility in global energy markets. Brent crude rose to $101 a barrel in the U.S. last week before easing to $98 following comments from President Donald Trump expressing optimism over a potential diplomatic resolution. However, uncertainty remains, with Iran signaling it is not currently engaged in negotiations.

Safaga–Duba Sees Surge in Activity

As a result, the Safaga–Duba route has recorded a sharp increase in traffic. Data cited by Al Ahram shows that between March 1 and March 15, 2026, the corridor handled 38 trips carrying 4,200 shipments and 105,000 tons of cargo, compared to 25 trips, 2,406 shipments, and 60,150 tons during the same period last year—an increase of 75% in exports.

Daily volumes now average 500 refrigerated containers and 12.5 thousand tons, supported by eight operating ferries. Al Arabiya described the surge as a renaissance, noting a 52% increase in trips in early March. Much of the activity is driven by transit trade, including fresh Egyptian produce and re-exported goods destined for Gulf markets.

A Structural Advantage — With Limits

Leheta highlighted the structural differences between disruptions in the Red Sea and Hormuz. “What tends to get overlooked is the difference between the two disruptions we are dealing with,” she said. “The Red Sea had a bypass. Ships rerouted around the Cape, added time and cost, and cargo kept moving. Hormuz does not work that way. When access is disrupted there, flows do not reroute. Jebel Ali handled 15.5 million TEU in 2024. That cargo has nowhere to go.”

Egypt’s geographic position—linking the Mediterranean, Red Sea, and overland Gulf access—has amplified the corridor’s importance. Freight volumes on the route have increased by 25% to 30% since the crisis began, according to Leheta, reflecting a direct commercial response to constrained Gulf access.

Private Sector ‘Partially Ready’

Despite the surge, Leheta cautioned that Egypt’s logistics ecosystem is not fully prepared to absorb sustained demand. “The honest answer is that the private sector is partially ready, and partial readiness is in some ways more dangerous than clear unreadiness, because it creates the appearance of capacity without the depth to sustain it under structural pressure,” she said.

She identified three key bottlenecks:

- Limited digital systems and truck handling capacity at Safaga port

- Weak backhaul economics, with trucks often returning empty

- Gaps in cross-border regulatory expertise among operators

Leheta added that nearly 90% of operators function informally, lacking the scale and compliance frameworks required by multinational clients.

From Transit to Value Creation

Looking ahead, Leheta stressed that long-term gains depend on capturing more value domestically. “My own assessment, held with appropriate uncertainty, is that the shift is partially structural and the structural component is larger than the market currently prices, but smaller than the most optimistic projections suggest,” she said.

She outlined a three-tier strategy: expanding warehousing capacity, developing value-added logistics services such as consolidation and phytosanitary processing, and integrating logistics with industrial zones to serve multinational manufacturers.

“Transit revenues are the least interesting part of this opportunity,” she added. “They are also the most fragile, because they are entirely contingent on the corridor remaining active under conditions that are not fully within Egypt’s control.”

Policy Over Infrastructure

Leheta emphasized that regulatory consistency, rather than infrastructure spending, is the key to sustaining momentum. “The single most critical requirement at this stage is not infrastructure. It is predictability,” she said, noting that delays of 24 to 48 hours can redirect major shipping flows.

She called for clearer bilateral frameworks with Saudi Arabia, expanded digital systems at Safaga, financing support for private operators, and stronger industrial zone integration. She also highlighted the need for centralized oversight.

“That gap between sectoral competence and systemic accountability is where Egypt’s logistics ambitions have historically stalled, and closing it would matter more than any individual infrastructure investment,” she concluded.